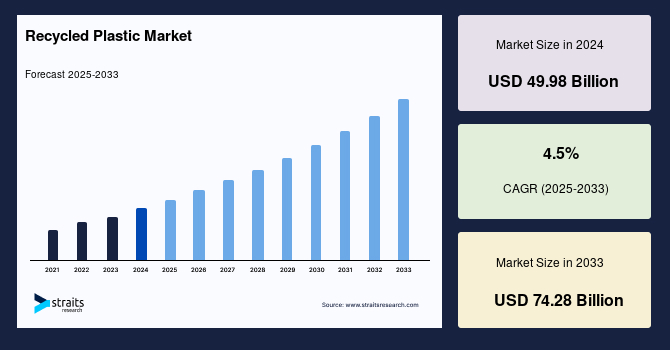

The plastics recycling sector is experiencing notable downsizing throughout Europe and the US, leading to demands for regulatory changes to tackle what is being described as market failure. Recyclers are confronting obstacles such as heightened competition from less expensive virgin plastics due to capacity increases in China and ambiguity surrounding policy as the sector shifts from voluntary to obligatory recycling targets. Escalating energy costs in Europe have heightened recycling expenditures, raising worries about fulfilling new governmental recycling objectives.

In Europe, the contraction is compounded by a lack of effective global agreements on limiting virgin polymer output, resulting in reduced volumes and outputs of recycled materials. Recent statistics indicate a decline in mechanical recycling capacity, marked by significant closures in the UK and the Netherlands. Recyclers stress the necessity for long-term agreements to lessen dependence on volatile virgin plastic pricing, with current policy holdups hindering the recycling demand essential for investment.

The EU’s Packaging and Packaging Waste Regulation (PPWR) aims to enhance packaging recyclability by 2030 and impose penalties for non-compliance, impacting even imported goods. While this intends to boost demand and encourage investment, the benefits will not be realized until 2030, leaving recyclers in financial uncertainty.

Meanwhile, the US is also implementing extended producer responsibility (EPR) laws that differ by state, potentially influencing brands’ commitments to utilizing recycled materials. To stimulate demand and improve supply chains, both incentives and penalties are proposed as mechanisms to foster industry engagement.

Significant variations in contamination levels, such as those seen in the UK, further complicate recycling initiatives. The UK’s dependency on exports and its relatively elevated contamination rates introduce additional obstacles. Export incentives through Packaging Export Recovery Notes (PERNs) contribute to this issue, despite attempts to enhance domestic recycling capabilities.

In the UK, recent legislative initiatives like the plastic packaging tax are intended to raise the recycled plastic content but have not sufficiently adapted to market dynamics. Current tax revenues indicate some uptick in compliance concerning recycled content, yet concerns regarding fraud persist, with some companies opting to pay the tax rather than utilize recycled materials.

Additional regulation, via the EPR framework and municipal waste incineration strategies, could potentially reroute plastic waste from incineration toward recycling, assuming that infrastructure development progresses steadily. The EU’s projected demand for recycled materials will necessitate considerable growth in chemically recycled plastics, requiring transparent accounting and compliance systems.

Ultimately, the effectiveness of these regulatory measures in promoting a circular economy will hinge on their capacity to cultivate an investment-friendly atmosphere that champions innovation and sustainability within the plastics recycling sector.